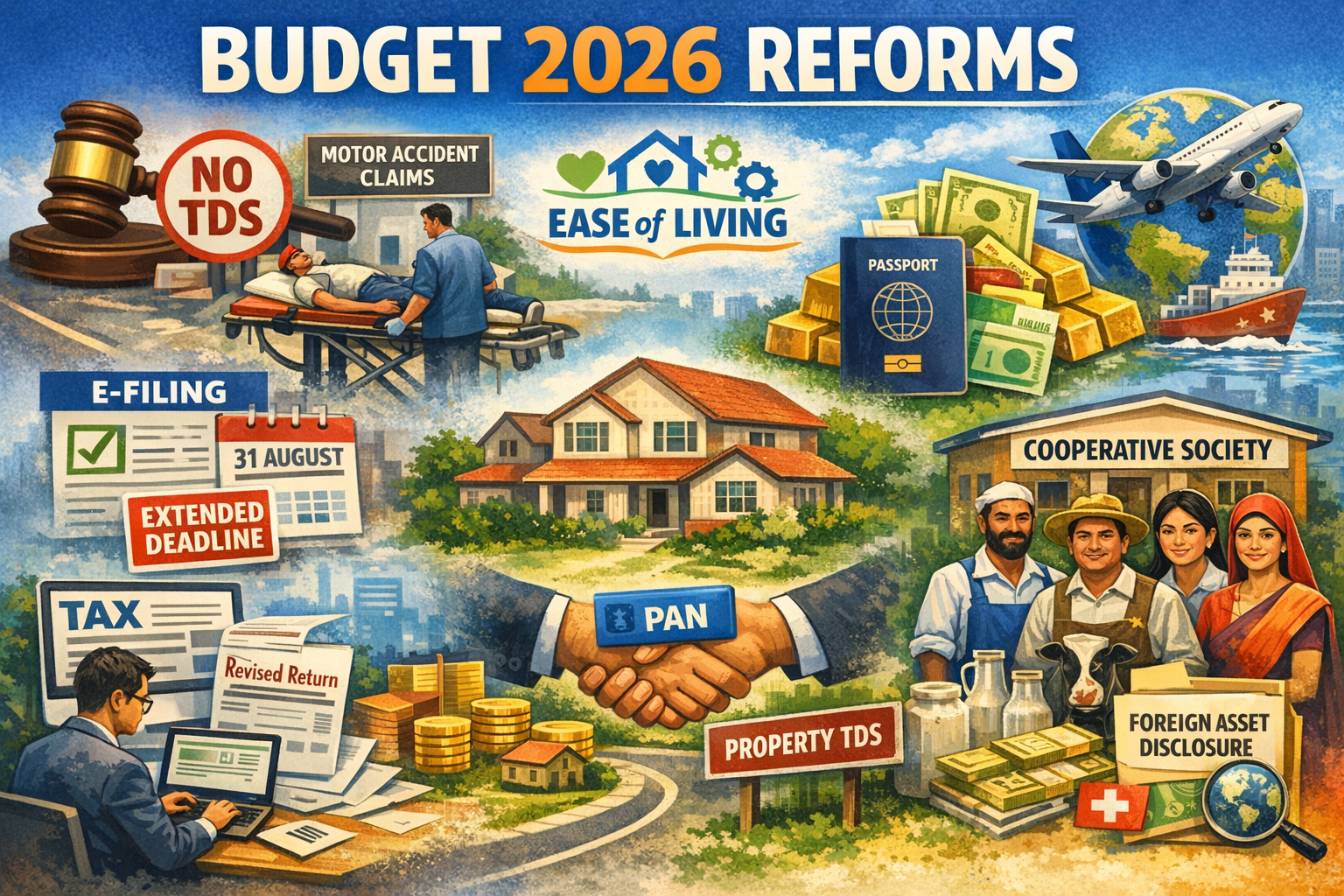

Budget 2026 Decoded: What the New Income-Tax Reforms Mean for Businesses, Professionals, and Cooperatives

Budget 2026 introduces one of the most compliance-centric and taxpayer-friendly overhauls in recent years. The reforms are not merely about tax rates—they are about reducing friction, simplifying procedures, digitising declarations, and making penalties proportionate.

For MSMEs, professionals, cooperative societies, startups, and investors, these changes materially affect how you deduct TDS, file returns, manage employee dues, handle property transactions, disclose foreign assets, and deal with penalties.

This article distills the most practical changes and what they mean on the ground.

Source reference: FAQs on Budget 2026 proposals

1) “Ease of Living” Translated into Real Compliance Relief

✅ No tax on MACT interest for individuals

Interest awarded by Motor Accident Claims Tribunal is now fully exempt for individuals/legal heirs. No TDS will apply.

✅ Manpower supply clarified under “work” for TDS

“Supply of manpower” is now explicitly treated as contract work for TDS. This removes disputes on whether 2% or 10% applies.

Impact: Staffing companies, security services, housekeeping contractors, HR vendors—TDS confusion ends.

✅ Easier lower/nil TDS certificates for small taxpayers

Applications can be made electronically to a prescribed authority instead of lengthy AO processes.

✅ Declarations for no-TDS can be filed with Depositories

Investors can file a single declaration with depositories for:

- Mutual fund income

- Securities interest

- Dividends

Depository shares this with all deductors.

Impact: No more submitting Form 15G/15H repeatedly to multiple entities.

2) Return Filing & Revised Return: More Time, Structured Fees

|

Change |

Earlier |

Now |

|

Revised return window |

9 months |

12 months |

|

Due date (non-audit businesses, trusts) |

31 July |

31 August |

|

Fee for late revised return |

Not structured |

₹1,000 / ₹5,000 slab |

Impact for MSMEs & trusts: Extra time to close books properly without panic.

3) Big Relief in Property Transactions (Especially with NRI Sellers)

Earlier, if you bought property from a non-resident, you had to obtain TAN to deduct TDS.

Now:

Buyer can deduct TDS using PAN only, same as resident cases.

Impact: Massive simplification for property buyers dealing with NRI sellers.

4) PF / ESI Employee Contribution: Long-Standing Pain Fixed

Earlier:

- Employer contribution allowed till ITR due date

- Employee contribution allowed only till PF/ESI due date (15th)

Now both aligned:

Employee contribution also allowed till ITR filing due date.

Impact: Huge relief for MSMEs and payroll-heavy companies.

5) Penalty → Fee, Prosecution → Proportionate Punishment

A philosophical shift:

- Many penalties converted to automatic fees

- Maximum imprisonment reduced from 7 years to 2 years

- Small tax defaults → fine only

- Several offences fully decriminalised

Impact: Less fear, more compliance, fewer litigations.

6) Updated Return Becomes a Powerful Correction Tool

Updated return (up to 48 months) gets expanded scope:

You can now:

- Reduce earlier claimed losses

- File updated return even during reassessment (with extra 10% tax)

- Avoid penalty for income disclosed via updated return

Impact: Encourages voluntary correction instead of litigation.

7) FAST-DS 2026: Foreign Assets Disclosure Window (Very Important)

A one-time scheme for small taxpayers:

|

Scenario |

Payable |

|

Undisclosed foreign asset/income ≤ ₹1 Cr |

60% of value |

|

Foreign asset acquired legally but not reported ≤ ₹5 Cr |

₹1 lakh flat fee |

|

Immunity |

From Black Money Act penalty & prosecution |

Who benefits?

- Employees with RSUs/ESOPs abroad

- Students with old foreign bank accounts

- Returning NRIs

- People with forgotten foreign insurance/balances

8) Rationalised Tax on “Unexplained” Income

Tax rate reduced from 60% → 30% on unexplained credits/investments.

Penalty now merged under misreporting provisions, with immunity option.

Impact: Encourages settlement rather than concealment.

9) Crypto Reporting Gets Teeth

Reporting entities must furnish crypto transaction statements.

Penalty:

- ₹200/day delay

- ₹50,000 for inaccurate reporting

10) Major Boost for Cooperative Societies

Several powerful changes:

- Multi-State Co-ops explicitly recognised

- Cotton seed & cattle feed added to eligible deduction supplies

- Inter-cooperative dividend deduction allowed in new regime

- Notified federations get dividend deduction for 3 years

Impact: Dairy, agri, seed, cattle-feed, and federal co-ops gain full deduction clarity.

What This Means for India’s MSME & Professional Ecosystem

Budget 2026 is not a rate-cut budget.

It is a compliance-simplification budget.

It reduces:

- Friction

- Ambiguity

- Fear

- Litigation

- Manual processes

And increases:

- Digital filings

- Standardisation

- Time windows

- Voluntary correction

- Ease for small taxpayers

Why This Matters for IndiaSEVA Community

IndiaSEVA connects:

- MSMEs

- Professionals

- Cooperative societies

- Exporters/importers

- Service providers

These reforms directly affect how you operate daily.

IndiaSEVA will continue to decode such policy changes into actionable understanding for category leaders.

If you are:

- A CA / CS / Tax consultant

- A cooperative federation expert

- A payroll / compliance specialist

- A property transaction advisor

- An NRI taxation expert

👉 We invite you to publish your practical interpretation on IndiaSEVA.com for the benefit of thousands of Indian businesses.